Subscribe if you want to be notified of new blog posts. You will receive an email confirming your subscription.

Healthcare Transformation: Coping With the Neutral Zone

I’m being asked the same series of questions a lot lately:

Do you think the changes occurring in US healthcare are real? Are we truly moving away from rewarding volume of care under fee-for-service (FFS) and toward value-based payment and delivery? Are the changes past the point of no return? Will the economic interests of the powers-that-be prevent real change from happening, just as they have done in the past?

The phrasing of these questions assumes a split, dichotomous view of the world — that change has/hasn’t yet happened. The questions also mask the underlying and difficult process of transition that people and organizations are going through.

There’s a different way to think about the transformation of U.S. healthcare — transition as a 3-stage process:

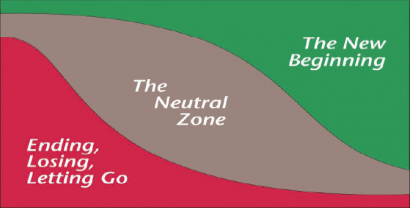

William Bridges 3 Stage Transition Model

Here’s a summary of where I’m going with today’s essay:

- Think of Transition as a 3 Stage Process

- U.S. Healthcare—Entering the Neutral Zone

- How Long Will the Neutral Zone Last? Quite a While.

- So What? What are Implications and Actions?

Think of Transition As a 3 Stage Process

The William Bridges Transition Model has been around for a while, and it applies to individuals as well as to organizations. Bridges has written several insightful books, including Transitions: Making Sense of Life’s Changes (focused on personal change and transition) and Managing Transitions: Making the Most of Change (focused on organizational change and transition).

The difference between change and transition is subtle, but important. Bridges describes change as “situational” (external) while transition is “psychological” (internal). Transition is a 3-phase, psychological reorientation that people and organizations go through in coming to terms with change:

- Ending — the need to disengage from old approaches, structures, relationships, roles, and accept moving on. At this stage people may experience fear, denial, anger, sadness, disorientation, frustration, uncertainty, a sense of loss.

- Neutral Zone—uncertainty and possible fear about what the future holds. People may experience mixed feelings — a resentment toward the change, low morale and productivity, anxiety, skepticism. The Neutral Zone can also be a time for creativity and growth.

- New Beginning—clarity about the future, acceptance and familiarity with the new reality. People will start feeling positive, re-energized, a renewed sense of purpose.

U.S. Healthcare—Entering the Neutral Zone

The people and organizations in the U.S. healthcare system today are predominantly entering the Neutral Zone — a time of confusion and discomfort. The Neutral Zone has been described as:

Limbo

No man’s land

“Linus when his blanket is in the dryer. There is nothing to hold on to.” Futurist Marilyn Ferguson

The Ending is upon us — a consensus is developing that fee-for-service healthcare is on the way out. A September 2013 McKinsey article — Claiming the $1 Trillion Prize in US Health Care— articulates the evolution:

As divisive as the debate has been, there is a clear consensus across political parties and health-care stakeholders that if the United States is to address its unsustainable health-care costs, it must change the way it pays hospitals, physicians, and other providers. The country needs to move away from fee-for-service reimbursement, which rewards providers for tasks performed, and toward a method of payment that compensates them for successfully addressing patients’ health-care needs.

The Ending is crystallizing. In the debate about whether fee-for-service healthcare is a good idea, there’s no one left in the room defending the Old World Order. In their silent heart-of-hearts, there are many hospital administrators and specialist physicians still hoping that the ruckus will all go away, but they are recognizing in their heads that this is wishful thinking.

The New Beginning, however, is cloudy and distant. While it’s clear that FFS must go and that we’re moving toward something called value-based care and delivery, the details are fuzzy. Clarity about a New World Order has yet to emerge.

There are many experiments under way with various value-based payment and delivery mechanisms — Medicare ACOs, commercial accountable-care-like initiatives, medical homes, bundling, coordination of care programs, readmission avoidance penalties, and others.

Which of these experiments will stick? We don’t know yet.

So here we are in the Neutral Zone. Stuck.

Bridges notes that the Neutral Zone is often thought of as a stage of “suffering and confusion.”

While that’s true, it can also be a time of great creativity, expanded thinking, and personal/organizational growth. While the tendency is to fight it, riding it out can be highly constructive and productive.

Given the complexity and the vastness of the U.S. healthcare system, it’s likely we’ll be in the Neutral Zone for a while.

But, how long?

How Long Will the Neutral Zone Last? Quite a While.

While we lack clarity about the details of the New Beginning, there are glimmers of consensus forming.

You might ask, “What’s a proxy or leading indicator of an emerging New Beginning?”

At least one key metric is emerging:

Non-Fee-For-Service (Non-FFS) revenue as a percentage of care provider revenue

At least four different analysts have examined this metric and offered perspectives about the transition. Let’s take a look at each. The short answer is that the pundits project that:

The transition away from FFS will take somewhere between 3 to 10+ years.

1) Catalyst for Payment Reform. Catalyst for Payment Reform (CPR) is a nationwide nonprofit organization led by employers and other health care purchasers committed to advancing payment reform. Representative members include AT&T, Boeing, GE, IBM and Wal-Mart.

Writing in a September 12, 2013 post in the Health Affairs Blog, Executive Director Suzanne Delbanco notes:

When Catalyst for Payment Reform (CPR) released its first-ever National Scorecard on Payment Reform last March, we faced some tough questions. The Scorecard revealed that just about 11 percent of payments to doctors and hospitals in this country are value-oriented, while the rest remain largely fee-for-service.

In The National Scorecard on Payment Reform CPR set a target of 20% of payments being value-oriented by 2020. Why did CPR set the goal of 20 percent by 2020?

In 2010, Catalyst for Payment Reform did an informal survey to assess how much payment was tied to provider performance and estimated that just 1-3 percent of payments to doctors and hospitals reflected their performance. Based on this, CPR set the goal of 20 percent of payments to doctors and hospitals being value-oriented by 2020. CPR Scorecard FAQ

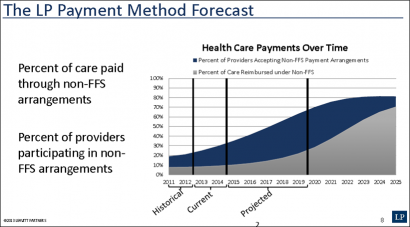

2) Leavitt Partners. Leavitt Partners (LP) is a “health care intelligence business”. The founder and Chairman is Michael Leavitt, former Secretary of Health and Human Services during the Bush administration. The LP Center for Accountable Care Intelligence collects, organizes and conveys information on ACO structural and operational models deployed throughout the country.

In a webinar summarizing Leavitt’s most recent report on ACO activity, they project that Non-FFS revenue will reach 50% of payments in about 2022 (slide 8).

3) McKinsey. In a September 2013 essay, Claiming the $1 Trillion Prize in US Health Care, the international consulting firm McKinsey opines that:

…with stronger leadership, bolder initiatives, and more collaboration between public and private payers, the US health-care industry could aggressively transition to outcomes-based payment over the next three to five years.

McKinsey got more specific in a February 2012 report, The Trillion Dollar Prize: Using Outcomes-Based Payment to Address the US Healthcare Financing Crisis:

…we believe that as much as 50% of healthcare payments could be outcomes-based by 2018

4) Availity. Availity provides health information solutions to a growing network that currently includes more than 200,000 physicians and providers of care, 1,000 hospitals, 1,300 health plans and 450 industry partners.

In a recent report — Provider and Health Plan Readiness to Support Value-Based Payment Models — the company shares finding from interviews with health insurance and care provider executives:

Limited revenue expected from value-based payments over the next year, but a significant shift is expected.

• In three years, 78% of physician practices predict the revenue they receive from value-based models will be between 15 and 50%.

• In three years, 52% of hospitals expect 25-50% of their revenue from value-based programs, with 36% anticipating 51-100% of their revenue from these models.

• Nearly 70% of all respondents expect to support three or more different value-based models in the next three years.

Caution: Availity acknowledges that the survey sample is small, and “study results are considered directional or observational.”

Let’s summarize the nuggets coming from these analysts:

Catalyst for Payment Reform: 11% of payments today are Non-FFS; CPR sets a goal of 20% by 2020

Leavitt Partners: Non-FFS will reach 50% of payments in 2022

McKinsey: as much as 50% of healthcare payments could be outcomes based by 2018

Availity survey: 52% of hospitals expect 25-50% of their revenue from value-based programs, with 36% anticipating 51-100% of their revenue from these models

Overall: 3-10+ years before Non-FFS becomes predominant

Some caveats here are appropriate. These studies do not make direct apples-to-apples comparisons. “Non-FFS” revenue is a broad metric and does not have a standardized definition. A reading of the sources cited above reveal many details and lessons being learned. Its likely that FFS will remain appropriate as payment for specific types of services.

So What? What are Implications and Actions?

We need to think and act differently about healthcare transformation.

Stop wondering whether change is occurring. It is. And it’s going to last.

Recognize that now we are in a chaotic, amorphous middle state — the Neutral Zone.

The real question now is not whether the change will occur, but when. The Neutral Zone is likely to last 3-10+ years, depending on which pundit you’d prefer to believe.

Non-FFS revenue is emerging as a consensus indicator of healthcare transformation.

There’s not likely to be a single, unified evolution of a New Beginning. Healthcare is still local.

We can all help the push toward the New Beginning. The rate of adoption of Non-FFS payment is not predetermined — it is a social phenomenon, not a geological or biological process. We can all make a difference.

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 Unported License. Feel free to republish this post with attribution.